China’s Industrial Policy & its Exponential Growth in the Global Shipbuilding Industry

Manu Bhat

March 10, 2026

Abstract

China’s exponential growth in the shipbuilding industry is quite spectacular, particularly in the magnitude of its operations compared to its peers. As such, it reduced its production costs by 13% to 20% between 2006 and 2012, disrupting the industry both locally and globally (Blanchette et al., 2025). This study examines how China’s state-driven industrial policy between 2006 and 2012 enabled substantial reductions in production costs, catalysed competitive disruption in global shipbuilding markets, and propelled the country’s swift rise to industry dominance.

Introduction

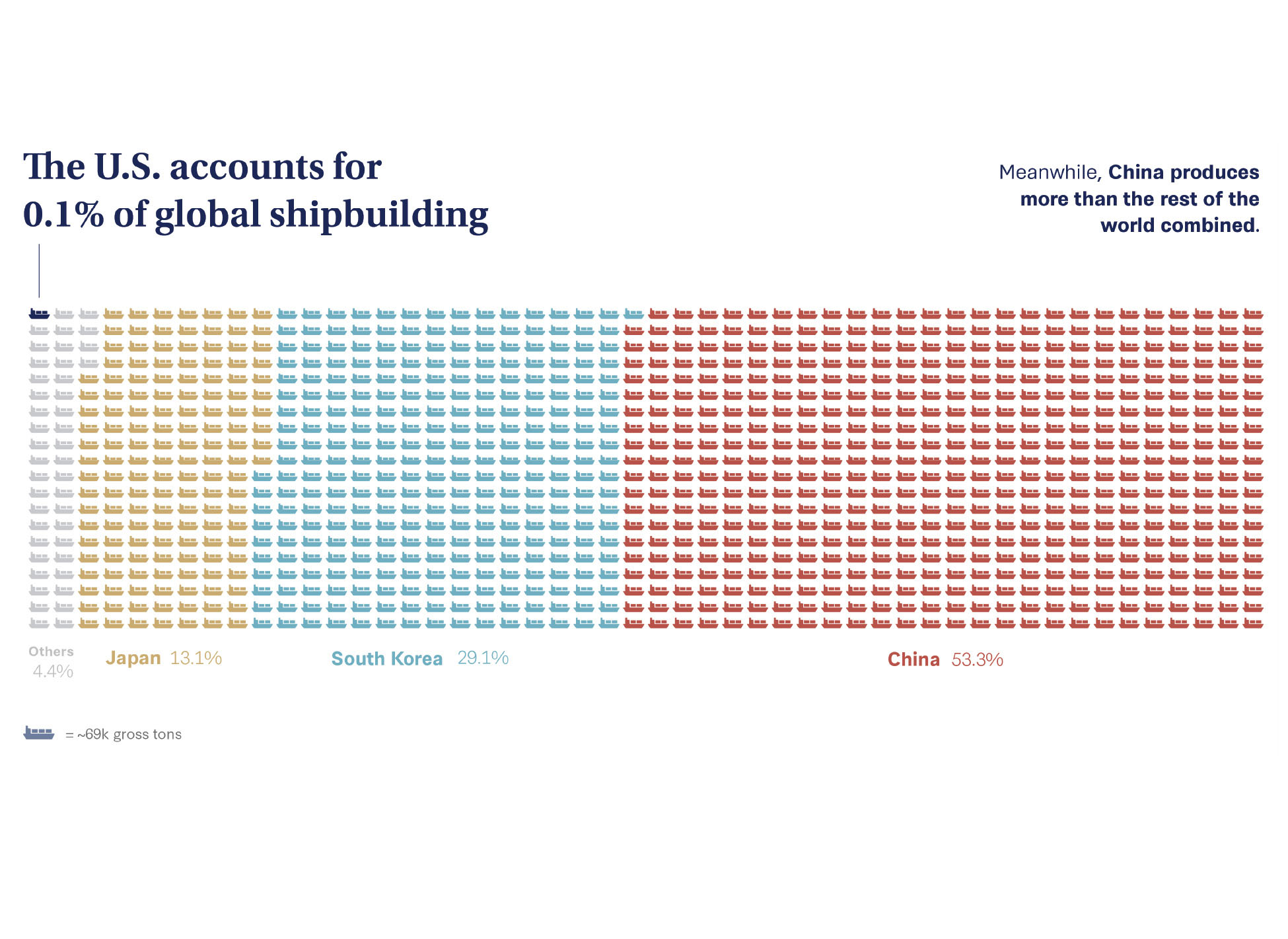

The global shipbuilding industry has historically been competitive, only dominated by a few key players. For decades, the powerhouses of East Asia, particularly Japan and South Korea, had maintained a lead in the production of commercial vessels. However, this historical dynamic was surgically dismantled by a strategic, state-led industrial policy aiming at supplanting global leaders. China had managed to grow in this area accounting for over 50% of the total market share, and cementing itself as the undisputed leader in the industry. From the dawn of the new millennium onwards (particularly from 2003 to 2008), the large-scale expansion achieved by the Chinese shipbuilders initiated growth, and, backed by favourable government policies, transformed this industry into a strategic export sector. While it had traditionally emphasised bulk carriers, tankers, and containers, China increased its production of specialised vessels, including gas carriers, offshore service vessels, passenger ships, car carriers, and roll-on/roll-off (ro-ro) vessels (OECD, 2021).

Source: (Funaiole et al., 2025)

Reports suggest that between 2000 and 2010, the Chinese shipbuilding production accounted for 37% of world completions and showcased a 31% CAGR (Compound Annual Growth Rate). The 2008 Financial Crisis had a negative impact on the ship demand from 2011 and further exacerbated the situation of the overcapacity problem. It eventually led to the merger between two of the largest shipbuilding State-Owned Enterprises (SOEs) in 2019, namely CSSC & CSIC. Another notable shock in the global value chains was during the outbreak of COVID-19, particularly in the first half of 2020, when ship deliveries from Chinese shipyards decreased by 22% in Compensated Gross Tonnage (CGT). Overall, with the possible exceptions of these setbacks and the overcapacity problem pertaining to this case, China has been able to keep its production constant, if not increase and optimize the supply chain. In 2024, Chinese shipyards captured 71% of global shipbuilding orders, securing 46.45 million compensated gross tons (CGT) (Han-kook and Su-hyeon, 2025). Seven of the top 10 shipbuilders by order volume came from China, according to data from Clarksons Research. Its ability to maintain production consistency, even during challenging circumstances, elicits that the resilience has been rooted in top-down state support.

Role of the Government

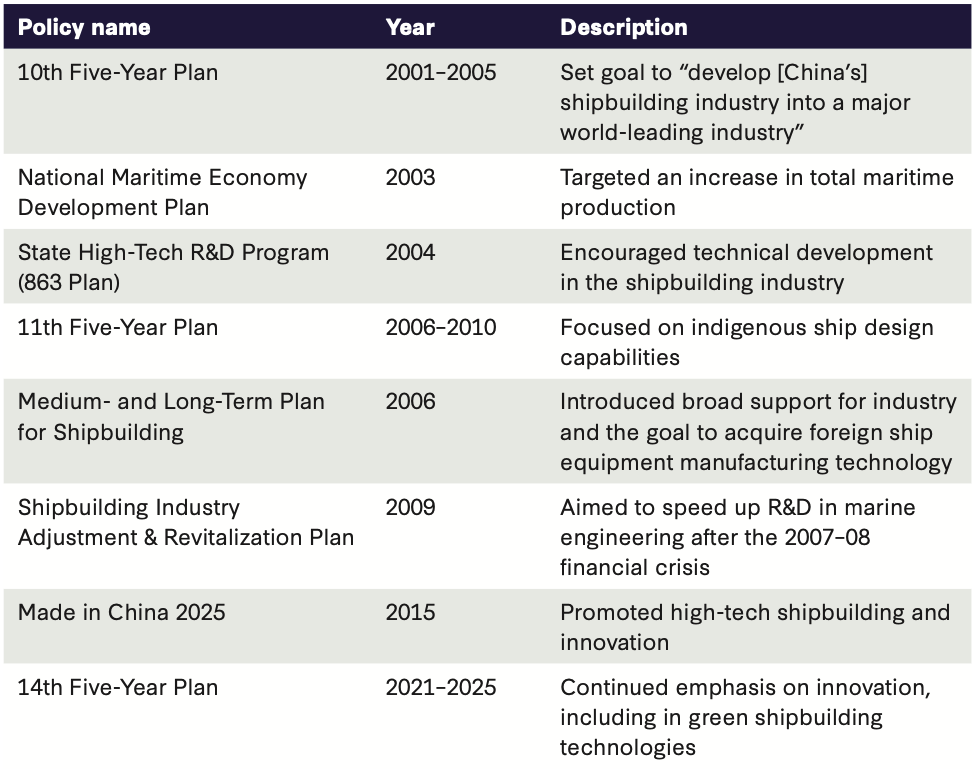

The emphasis given to the shipbuilding industry by the Chinese government is evident in the title “Pillar Industry” designated to it in both the 11th (2006-10) and the 12th (2011-15) National 5-Year Plans (Funaiole et al., 2025).

Source: (Funaiole et al., 2025)

Between 2005 and 2015, the cumulated oversupply reached 297 million gross tonnes in total and accounted for 23% of the world fleet in 2015 (OECD, 2021). This situation has remained particularly severe for most large vessel categories, such as tankers, bulkers, and containers. Future vessel requirements that were expected to be equal only in 2030, at the peak of completions, were actually reached in 2011 (OECD, 2021). However, Chinese industries paradoxically benefited from the artificially low-priced steel and other critical inputs due to the overcapacity in the upstream industries, which acted as a hidden subsidy. They also faced (and still face) the problem of ‘Zombie’ SOEs—state-owned firms kept alive despite chronic losses through state support, all of which led to the overestimation of the industry competition. The approach of the Chinese government to the overcapacity problem was the expansion of both its fiscal policy and monetary policy, aimed not at reducing capacity but at managing the problem for strategic advantages in the long run. China allocated CNY 100 billion in 2016 to support local governments in addressing the impact of capacity reductions on employment and provided CNY 2 billion in 2019 (approximately USD 300 million) to reduce overcapacity in key industries through rewards and subsidies. Subsequently, Party Committee members of central SOEs were encouraged to implement the Party’s ideology about dwindling excess capacity and zombie firms.

However, the inadmissible advantage that the Chinese possessed and enjoyed in comparison to their counterparts was not the relatively small grants but essentially the favorable state-led financial mechanisms and the opaque long-term financing from state banks such as the China Export-Import Bank (China Exim) and the Bank of China. According to a CSIS analysis, combined state support to Chinese firms in the shipping and shipbuilding industry totaled roughly USD 132 billion between 2010 and 2018 (Blanchette et al., 2025). They included strategies such as the availability of cheaper credit facilities, subsidies of various scales (Production, Investment & Entry Subsidies), Insurance Premium Compensation, Financial Leasing, Debt-Equity Swaps, Guarantees, Tax Rebates & Incentives, Vessel Demolition Subsidy Scheme, Legal support, and R&D initiatives. Reports by NBER elucidate strong evidence that government subsidies directly reduced the cost of production in Chinese shipyards by 13% to 20%, corresponding to an estimated value of USD 1.5 billion to USD 4.5 billion between 2006 and 2012 (Kalouptsidi, 2014). Cumulatively, all of these facets of State support accounted for one of the most fundamental reasons why China has been able to position itself as a leader in this paradigm.

References:

Blanchette, J., Hillman, J. E., Qiu, M., & McCalpin, M. (2025). Hidden harbors: China’s state-backed shipping industry. Center for Strategic and International Studies. https://www.csis.org/analysis/hidden-harbors-chinas-state-backed-shipping-industry

China shipbuilding industry report 2025: Global leader in completions, orders, and exports. (2025, July 24). VesselsLink. https://vesselslink.com/blogs/news/china-shipbuilding-industry-report-2025-global-leader-in-completions-orders-and-exports.

Funaiole, M. P., Hart, B., & Powers-Riggs, A. (2025). Confronting China’s dual-use shipbuilding empire. Center for Strategic and International Studies. https://www.csis.org/analysis/ship-wars-confronting-chinas-dual-use-shipbuilding-empire

Han-kook J. & Su-hyeon P. (2025). China dominates global shipbuilding in 2024, capturing 71% of orders. The Chosun Daily. https://www.chosun.com/english/industry-en/2025/01/27/MPCPWLMZRBABTK4XF3KJ56RYPI/

Kalouptsidi, M. (2014). Detection and impact of industrial subsidies: The case of world shipbuilding (NBER Working Paper Series, No. 20119). National Bureau of Economic Research. https://www.nber.org/system/files/working_papers/w20119/w20119.pdf

Organisation for Economic Co-operation and Development. (2021). Report on China’s shipbuilding industry and policies affecting it. (OECD Science, Technology and Industry Policy Papers, No. 105). OECD Publishing. https://doi.org/10.1787/bb222c73-en

U.S. Trade Representative. (2024). China’s targeting of the maritime, logistics, and shipbuilding sectors for dominance; (Investigation Report). https://ustr.gov/sites/default/files/enforcement/301Investigations/USTRReportChinaTargetingMaritime.pdf